Blog

How to Calculate and Improve Your Days Payable Outstanding (DPO)

23 Sep

Products

Axtension for F&O

Solutions

By Process

By Feature

By Role

By Industry

Partners

Resources

About us

Blog

23 Sep

The speed at which a company pays its suppliers has ripple effects on cash flow, financial strategy, and vendor trust. Days payable outstanding (DPO) shows exactly where an organization stands, and improving it can unlock both operational efficiency and stronger supplier relationships.

Let’s review how to calculate DPO correctly, its importance with the AP function, and strategies to optimize your processes.

Key highlights:

Days payable outstanding is used to calculate how many days, on average, an enterprise takes to pay suppliers after they receive an invoice. The calculation is made by dividing average accounts payable by cost of goods sold (COGS) and then multiplying it by 365. The result shows how long, on average, cash stays in the business before being paid out.

Every payable decision affects more than the immediate invoice, altering cash availability, signaling financial discipline to stakeholders, and influencing the company’s operating flexibility. When done correctly, calculating days payable outstanding becomes a lens to evaluate both liquidity and financial strategy.

Here are the top reasons why it’s critical for enterprises to have a handle on their real-time DPO:

Working capital equals current assets minus current liabilities. Days payable outstanding determines how long cash tied to payables remains available before it leaves the business. A high DPO defers outflows, especially when compared to days sales outstanding (DSO), the measure of how efficiently your accounts receivable function is working to collect money from customers.

If collections occur sooner than payables are due, the business gains a cash window it can use for operations, payroll, or debt service. To keep working capital aligned with needs, finance teams should set DPO targets, audit inputs such as AP aging reports and supplier master data, and monitor results against budgeted assumptions.

According to a SAP survey, 51% of suppliers report that buyers are typically late with payments. Delays beyond contracted terms can damage vendor relationships and create long-term consequences that impact the future-facing costs of doing business.

Meeting agreed terms demonstrates reliability, builds trust, and can secure benefits such as better pricing or priority on limited inventory. Consistently stretching DPO, however, may raise supplier concerns and result in stricter credit conditions, prepayment demands, or higher costs.

Accurate DPO calculation enhances budget planning by clarifying when you actually need to pay for goods and services. Knowing the average settlement period for payables allows finance teams to align disbursements with expected inflows and manage cash reserves more effectively.

Mapping payable into short-term forecasts, such as a 13-week cash flow, gives finance visibility into when invoices actually convert to payments. Factoring in delays from invoice coding errors, missing purchase orders, or exception queues improves forecast accuracy and helps AP teams anticipate liquidity needs more precisely. For example, tracking unmatched POs in Dynamics 365 that often push payments into the next cycle, or invoices on hold pending coding corrections.

According to data from the American Productivity & Quality Center (APQC), the average DPO across all industries is about 40 days. Individual results, however, vary widely by sector, business model, and company size.

Comparing your own calculation against peers provides context for whether payables are being managed effectively or signaling potential risk. For example, manufacturers with large supplier bases often sustain longer-lead payment terms than service providers with fewer vendors. Benchmarking should emphasize medians and quartiles rather than single averages, and your team should track results over time to identify shifts.

Several variables influence how DPO is calculated and interpreted.

| Factors That Affect Your DPO Calculation | Impact on DPO |

|---|---|

| Payment Terms and Policies | Longer contractual terms increase DPO, while shorter terms decrease it |

| Supplier Relationships | Strong vendor trust can allow extended payment cycles, while weak relationships often shorten them |

| Industry Standards | Industries with slower turnover, like manufacturing, typically show higher DPO than fast-cycle sectors like retail |

| Company Size and Resources | Larger firms often negotiate longer terms and higher DPO, while smaller companies face shorter terms |

| Seasonal Business Fluctuations | Busy seasons may extend payables and raise DPO, while slow periods usually shorten them |

The standard days payable outstanding formula is: (Average Accounts Payable ÷ Cost of Sales) × 365.

To get a better understanding of the DPO formula, let’s take a look at the calculation in action using Apple’s publicly reported accounts payable figures gathered from FinBox.

Apple reported accounts payable of $50.374 billion in 2024 and $47.574 billion in 2023, giving an average of $48.974 billion. Dividing this by $217.9 billion in cost of sales and multiplying by 365 gives a DPO of 82 days.

This result shows Apple keeps cash in the business for nearly three months before paying vendors. Benchmarks provide practical context: Lenovo averages 71 days, Dell 118 days, and HP 137 days. Apple’s figure sits between these peers, showing how approaches to managing payables differ even within the same industry.

DPO is a straightforward ratio, but missteps in sourcing or interpreting the data can distort results and mislead decision-making. Here are the four most common errors finance teams encounter, and practical ways to prevent them.

DPO is only as reliable as the numbers feeding it. Errors often result from simple missteps, such as using total expenses instead of cost of sales, or failing to average accounts payable over two periods. Seemingly minor mistakes in data entry can inflate or understate the result and lead to poor decisions. To avoid these DPO issues, teams should:

A common DPO calculation mistake is comparing figures from mismatched reporting periods, for example, using quarterly payables data against annual cost of sales. A misalignment can skew the ratio and produce misleading outcomes. To maintain consistency:

High or low days payable outstanding values are not inherently good or bad. A high figure might reflect a deliberate working capital strategy, or it could indicate that invoices are stuck in exception handling with missing approvals. For instance, a backlog of supplier invoices that is waiting for three-way match clearance or is stuck in exception queues.

To better understand high or low days payable outstanding values, AP teams need to:

DPO often shifts during high-demand periods, and ignoring these patterns produces misleading results. Retailers, for instance, may extend payables during holiday seasons but shorten them during slower months. To account for these fluctuations, businesses should:

Organizations looking to shorten their payables to improve DPO can focus on the following approaches:

Improving days payable outstanding requires more than one-time adjustments. It takes ongoing discipline, alignment with strategy, adjustments to AP workflows, and clear communication with suppliers. The following four DPO best practices help organizations support financial health and operational stability:

Targets should reflect industry norms, company size, and supplier mix. Too high can strain relationships; too low can reduce available working capital. To establish the right baseline, ensure that you:

Supplier trust depends on predictable, fair payment practices. Stretching DPO beyond agreed terms may save cash, but risks vendor confidence and stability. To keep relationships strong while managing payables:

DPO should be tracked alongside other working capital metrics to give a complete picture of financial efficiency. To make monitoring practical and actionable, you should:

DPO policies should serve long-term goals, not just short-term cash needs. Misalignment can undermine debt management, short-term investments, or growth objectives. To align DPO with broader financial planning, ensure you:

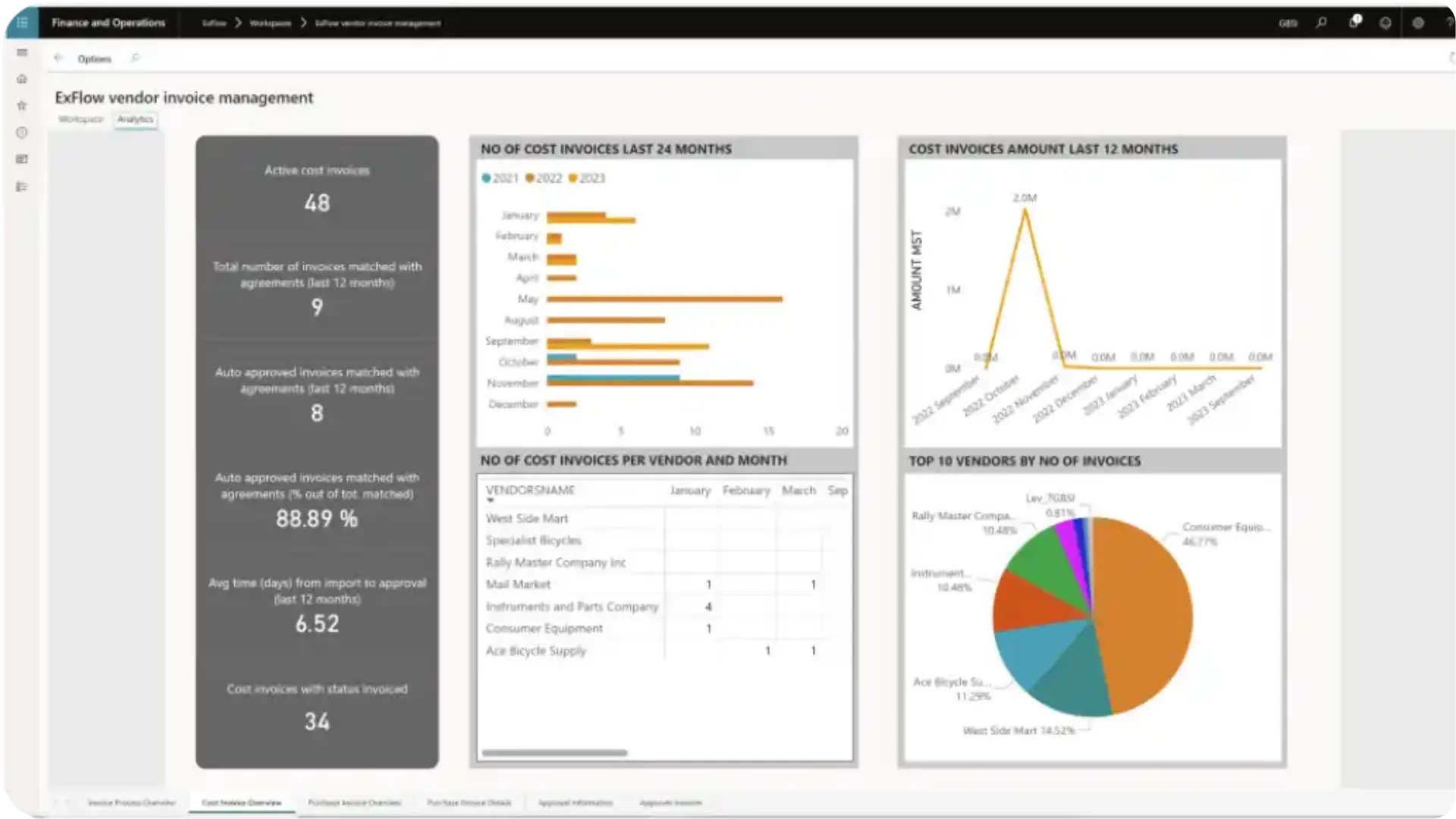

ExFlow offers a direct path to enhancing DPO through automated invoice management, which eliminates bottlenecks in the AP process. Fully integrated into Microsoft D365 for Finance & Operations and Business Central, it delivers real-time visibility into payables and cash forecasts, helping finance teams optimize payment schedules without overextending supplier terms.

Key ExFlow features include:

Book a demo today and explore how ExFlow can help your organization reduce days payable outstanding.

Days sales outstanding (DSO) measures how quickly a company collects payments from customers, while DPO measures the average number of days it takes to pay suppliers. Together, they reveal the timing gap between inflows and outflows, shaping working capital efficiency and overall cash conversion cycle performance.

Calculate days payable outstanding at least quarterly to align with financial reporting, though monthly reviews provide more actionable insight. Frequent tracking helps identify shifts caused by seasonality, policy changes, or supplier terms, ensuring results are reliable and helpful in managing cash flow and vendor relationships.

There is no universal “good” days payable outstanding calculation. Appropriate values depend on industry norms, company size, and supplier agreements. For context, APQC data show that the cross-industry average number of days between invoice and supplier payment is 40; however, manufacturing or technology firms may sustain much higher figures without signaling financial risk or supplier strain.